We would like to inform you about the latest tax changes and saving opportunities with this end-of-year newsletter. We hope you will benefit from this newsletter. Please contact our office for more information and personal advice. We have distinguished our tips and hints between private and business. Please go ahead and read what applies to your situation!

With kind regards,

J.C. Suurmond & zn. Tax consultants

Trusted advisors since 1986

Untaxing taxes!

Tax Plan Summary

This is the first budget of the new Rutte IV government, which, as expected, incorporates many of the plans in the coalition agreement. In addition, a number of changes from the ‘Voorjaarsnota’ (Spring Memorandum) have been included in response to budgetary challenges due to, amongst others, the consequences of the war in Ukraine and the Supreme Court decision for box 3.

The box 1 Income Tax is reduced slightly. This is offset by a number of other increases in, for example, the property transfer tax and Box 3 levy for second homes. Corporate income tax for Ltd’s will also be increased, reversing earlier cuts. There has been much talk this year about the box 3 levy following the Supreme Court’s Christmas ruling with significant implications for the way it is levied. You can read more about it below, both about the corrections over previous years and what the situation looks like from now on.

A selection of some tips before the end of this year:

– If you still want to make use of the increased gift exemption of €100,000 for your child’s own home, this is possible until 31-12-2022 at the latest. Under certain conditions it is possible to spread the actual payment over 2022 and 2023.

– The new box 3 levy is based on different asset categories; you could possibly take advantage of this by adjusting the composition of your assets before 31 December. This could include, for example, converting low-yielding investments or loans (receivables) that are currently taxed at the highest rate to low-taxed savings.

– For 2023, the rate of income tax deductions for higher-income earners will again be reduced with 3%; if it is possible to bring deductible expenses forward, the deduction will yield more this year.

Index individuals tax tips:

Changes box 1 Tax – Income from work and first-residence property

Supreme Court ruling and corrections box 3 levy

‘Mass appeal’ for non-objectors box 3 tax

Box 3 calculation – levy on foreign property

Changes 2023 Box 3 – Benefit from savings and investments

Limitation to shifting between box 3 categories

Reduction in the rate of deductible items for higher incomes

Limitation of 30% ruling for high wage earners

Increasing taxation on second property

Last chance for high tax-free gift ‘jubelton’

Replacement deduction for training costs

Other tax tips

Index business tax tips:

Change in corporate tax

Change in box 2 tax- income from substantial shareholdings

Tax-free allowances employees

Tax free scheme

Termination of efficiency margin for usual wage

Restriction on borrowing from own company

Loss relief corporate income

Bills to prevent tax avoidance for international companies

UBO register temporarily out of public access

Other tax tips

Individuals tax tips

Changes Box 1 Tax – Income from work and first-residence property

In 2023, the rate in the first bracket will be reduced from 37,07% to 36,93%. The threshold for the first bracket has also been raised this year, from € 69.398 to € 73.071. The rate for the second bracket remains 49,50%.

Income Tax – AOW not reached

2022

Income Tax – AOW not reached

2023

First bracket up to € 69.398

37,07%

First bracket up to € 73.071

36,93%

Second bracket from € 69.398

49,50%

Second bracket from € 73.071

49,50%

A three-bracket system still applies to taxpayers who have reached the state pension age. Disc 1 goes from 19,17% to 19,03%. The second bracket goes from 37,07% to 36,93% and the third bracket remains 49,50%.

Income Tax – AOW reached

2022

Income Tax – AOW reached

2023

First bracket up to € 35.472

19,17%

First bracket up to € 37.149

19,03%

Second bracket: € 35.472 – € 69.398

37,07%

Second bracket: € 37.149 – € 73.071

36,93%

Third bracket from € 69.398

49,50%

Third bracket from € 73.071

49,50%

*other brackets apply to people born before 1 January 1946

For box 2 rates, please refer to the business section of the newsletter.

Supreme Court ruling and corrections box 3 levy

Legal proceedings have been going on for years about the fictitious way of levying tax on the box 3 capital. After all, a fictitious return was assumed that was many times higher than that received on the savings account. The rulings for previous years however all turned out negatively for taxpayers. Ultimately, however, the Supreme Court ruled last December that the fictitious calculation of box 3 for the years 2017 and 2018 can be disproportionately burdensome and therefore in violation of the human rights treaty. According to the Supreme Court, legal redress must be offered to taxpayers who have objected.

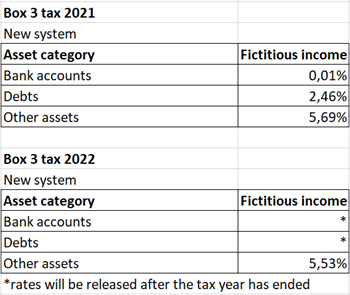

The Tax Office has worked out this correction of taxes by taking into account the actual composition of their assets and not the fictitious progressive rates. A fictitious return is still assumed; the return on savings has been sharply reduced to 0,25% or less based on actual interest rates. However, the highest percentage of around 5,5% applies to all other assets. A lower percentage of around 3% applies to debts. The tax-free allowance is calculated at a weighted average rate. In any case, generally this will provide a better connection to the actual wealth situation. Since the fictitious return on other capital is calculated based on the highest percentage, the new calculation is not necessarily more favourable in all situations. However, if this turns out to be less favourable, the existing box 3 calculation will remain in effect. From 2023, only the new system will be applicable.

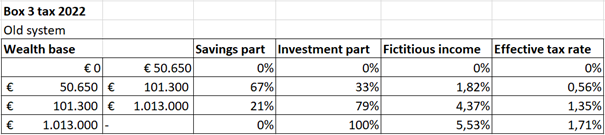

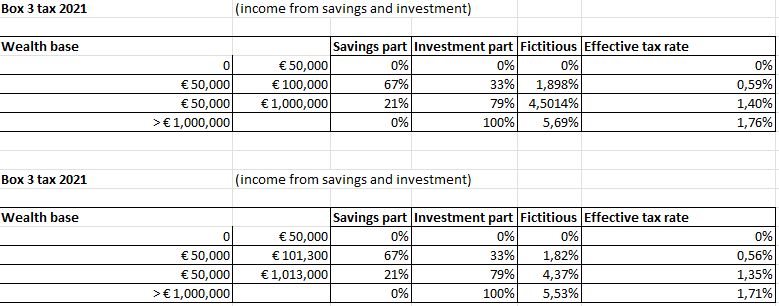

Below is an overview of the old box 3 tax system in 2022.

‘Mass appeal’ proceedings for non-objectors box 3 tax

It was announced on the 4th November that a supplementary procedure, ‘massaal bezwaar plus’, will be set up for non-objectors. If it follows from this appeal procedure that non-objectors are eligible for legal redress, this restoration will take place in the same way as for objectors. Taxpayers will then no longer have to make an individual request. By doing so, the Tax Office wants to prevent large numbers of appeals being filed again. This mass appeal procedure specifically is for those who did not timely submit an appeal. If you have lodged an appeal, but still do not agree with the outcome for other reasons, we recommend you do submit a request. This may concern, for example, the allocation between partners or the calculation of the levy on foreign property. For the year 2017, this request will have to be submitted before the end of 2022. For more details about this, please contact our office. If you have any questions about this, please contact our office.

Box 3 calculation – levy on foreign property

Incidentally, there are some ambiguities regarding the calculation of the double taxation deduction on foreign real estate. In our view, the deduction was calculated in an unfavourable way, assuming the average rate instead of the high rate applied to real estate. The Tax Office has since started correcting the previous deductions itself. In addition, the choice between the old or the new system is also not unambiguous in situations involving double taxation deductions. We recommend checking these cases extra carefully and raising an appeal if necessary.

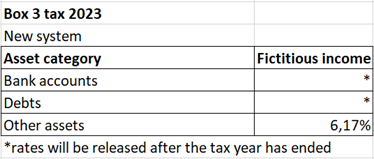

Changes 2023 Box 3 – Benefit from savings and investments

From 2023, the new box 3-system will apply. Under this system, the categories of savings, other assets and debt each have their own percentage of notional return. In 2023, the tax-free wealth will be increased to around € 57.000 (€ 114.000 for tax partners). Based on the asset mix, an average return is calculated on the total assets. The rate on the notional return in box 3 will be 31% in 2022. This rate will be gradually increased annually by 1% to 33% in 2024, thus reaching 32% in 2023.

It is planned to introduce a tax system based on actual returns and capital gains by 2026. This follows the Supreme Court’s ruling on the notional return; however, in practice, there are many snags in any system. Consequently, much is still unclear about the new box 3 tax, and it remains to be seen whether it will actually be introduced in 2026.

Limitation to shifting between box 3 categories

Under the new system of box 3 taxation, savings are taxed more favourably than other assets. To prevent taxpayers from shifting their assets between the different asset categories just around the tax reference date for box 3, a provision has been included in the Box 3 Bridging Act. If a transaction falls within a three-month period around January 1, it is ignored for the purpose of calculating the box 3 tax on 1 January. Therefore, due to this provision, temporarily converting assets does not result in lower taxation. If the conversion, for example from investments to savings, was more than three months ago at the time this conversion is reversed, it does not fall under the reference date arbitrage limitation. If the transaction is not for tax reasons then this also does not fall under the reference date arbitrage; for this, the tax authorities can request documentary evidence to establish this. The first reference date of the new system is 1-1-2023.

Shifting between asset categories around the reference date of 1 January is therefore, in principle, only successful if the shift is maintained for three months. Of course, costs of transferring securities and other assets should also be taken into account. Do you have any questions about this arrangement? If so, please contact us.

Reduction in the rate of deductible items for higher incomes

As already mentioned in 2020 and 2021, the highest rate at which virtually all deductible items are to be deducted is gradually being decreased. It can therefore be advantageous to bring forward deductible costs where possible. Taxpayers whose income falls in the highest bracket in box 1 will gradually have less tax advantage from these deductible items. In 2023, these deductible items may be deducted at a maximum of 36,93%, compared to 40% in 2022.

This concerns the following deductions:

Alimony

Deduction of study costs

Deduction of expenses for specific healthcare costs

Deduction of weekend expenses for disabled

Gift deduction

Mortgage interest deduction

Entrepreneurial deduction (self-employer’s deduction, research and development deduction, cooperation deduction, starter’s deduction in the event of incapacity for work, discontinuation deduction)

Profit exemption for small and medium sized businesses

Due to this reduction, the deductible items will yield more in 2021 than in 2022 and the following years. If your income falls in the highest tax bracket in 2021, it is therefore advisable, if possible, to pay deductible items such as gifts or healthcare costs before the end of the year.

Limitation of 30% ruling for high wage earners

The 30% rule for incoming employees will be limited to the WNT norm(also known as the Balkenende norm) from 1 January 2024. In 2022, this norm will be €216.000 on an annual basis and in 2023 €223.000. There is a transitional arrangement for incoming employees for whom the 30% rule was applied over the last pay period (December) of 2022. For existing 30%-ruling cases the capping of the 30% rule only applies from 1 January 2026, instead of 1 January 2024. So if you were planning to hire an incoming employee with a salary above the WNT norm early next year, the employee will benefit from an additional two year if the employment starts already as of 1 December 2022. Please contact us for advice on the possibilities.

Increasing taxation on second property

From 1 January 2023 the property transfer tax when buying a second property, will be raised to 10,4%. Until now this rate was 8%. Furthermore from 2023 onwards the correction that was possible based on the rental status of a second property will be limited. Whereas until 2022 the value could be reduced to 45% of the WOZ-value, from 2023 onwards this will be a maximum of 73%. If you would like to know how this will work out in your situation please contact our office.

Last chance for high tax-free gift ‘jubelton’

In 2022 it is your last opportunity to donate the so-called ‘jubelton’ of € 106.671 to your child or anyone other person tax-free. The condition is that the receiver spends this amount on an own home within 3 calendar years and that he or she is between 18 and 40 years old on the date of the gift. From 2023, this exemption will only be €37.231.

The general annual gift exemptions are yet available to be made use of this year. Please note that the money must be credited to the recipient’s account by December 31, 2022 at the latest. There is a general exemption of € 2.274. An exemption of € 5.677 applies to gifts to children. In addition, there are a number of one-off gift exemptions (for example, for a study or the purchase of a primary residence). If you have any questions regarding these exemptions, we will be happy to assist you.

Replacement deduction for study costs

From tax year 2022 onward, study costs are no longer deductible from the income tax. The tax deduction will be replaced by the STAP budget subsidy scheme (Incentive for the Labor Market Position). This budget will apply to people with a link to the Dutch labour market. From 1 March 2022, workers and job seekers can apply for a STAP budget at the UWV. This is possible per person once a year. The budget is €1.000 per person per year. If the application is approved, the amount is paid to the trainer. Only study costs paid until 2021 can still be deducted in the Income tax returns.

Other tax tips

Do you expect to pay tax for the 2022 or 2023 tax year? Requesting a provisional assessment in good time, will save you legal interest. Interest is calculated if the assessment is imposed later than 6 months after the end of the calendar year (1 July 2023). The tax interest is at least 4%. To ensure that the assessment is imposed in time, we recommend that you apply for it before 1 April 2023. The assessment for the 2022 tax year must be paid at once. There is the possibility of paying the assessment for the tax year 2023 in instalments. Do you have questions about this? We are happy to assist you in applying for a provisional assessment.

If you expect to receive a refund for 2017, an Income Tax return for this year must be submitted before December 31, 2022. In 2023, the 5-year term for submitting this declaration will expire.

If possible, bundle deductible expenses such as medical expenses and donations in one specific year. For example, a deduction is achieved earlier and the threshold is only deducted once from the expenses. For donations, the threshold disappears completely if you commit the donation to a charitable institution for 5 years.

The income-related combination discount can be applied to people with children under the age of 12. The conditions are that both partners work. The income-dependent combination discount will be increased to € 2.694 in 2023. From the 1st January 2025, the income-related combination discount will be abolished. Children born before this date will still be entitled to this tax credit for 12 years. However, there is still talk of a transitional arrangement, the outcome of which is not known at the moment.

Business tax tips

Change in corporate tax

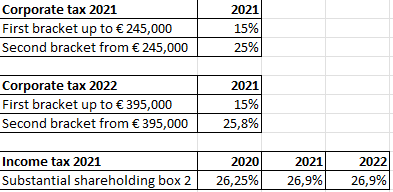

The corporate tax rate will be increased this year. Apart from that, the tax brackets are also modified. The corporate tax rate was 15% on the first €395.000 profit and 25,8% for profits above € 395.000 this was 25% in 2021. In 2023, the rate will be 19% on the first € 200.000. The rate for profits above € 200.000 remains 25,8%.

Corporate tax 2022

2022

First bracket up to € 395.000

15%

Second bracket from € 395.000

25,8%

Corporate tax 2023

2023

First bracket up to € 200.000

19%

Second bracket from € 200.000

25,8%

Changes in box 2 tax – Income from substantial shareholdings

The box 2 rate remains unchanged at 26,9% for 2023. A two bracket tax rate will be introduced in box 2 from 2024. This concerns income from substantial shareholdings, such as dividends and capital gains on shareholdings above 5%. The rate in 2024 will be 24,5% for the first €67.000 and 31% for the amount above that. Since this applies per partner, a total of € 134.000 can be taxed at the low rate in case of tax partnership.

Income tax box 2

2022 and 2023

Income tax box 2

2024

Flat rate

26,9%

First bracket op to € 67,000

24,5%%

Second bracket fron € 67,000

31%

Tax-free allowances employees

Because many people have been working from home since the corona crisis (and this indirectly costs the employee money; more energy consumption, coffee consumption, etc.), the cabinet has decided to introduce a tax-free working from home allowance. As a result, employers can reimburse a maximum of € 2 per day or part of a day worked. The tax-free travel allowance of € 0,19 per km will continue to exist and will be raised to € 0,21. The allowances cannot be paid at the same time; per day you can either opt for payment of the work from home allowance, or payment of the travel allowance.

An employer can provide a tax-free allowance for setting up a home workplace. The employer can reimburse the costs for, for example, an office chair or computer screen via other specific exemptions from the work-related costs scheme.

Tax free scheme

We would like to make you aware of the possibility under the Dutch Wages Tax Act to make a payment on a tax free basis for certain reimbursements which normally would be regarded as taxable income. This year this tax free scheme (‘vrije ruimte’) is maximised at 1,7% of the total company wages up to € 400.000,– and 1,18% beyond that. If you have not paid any other reimbursements or benefit in kind to employees including directors which could be regarded as taxable wage, you could still make use of this scheme by paying out a tax free bonus. An amount up to maximally € 2.400 would be seen as common. A temporary widening to 3% over the first €400.000 of the wage bill applies for 2023. This is reduced again from 2024 to 1,92% of the wage bill up to € 400.000.

Termination of efficiency margin for usual wage

Director-major shareholders (>5% shareholding in a BV) are subject to the customary wage scheme. In 2022, the salary could in principle be set 25% lower than what was customary for employees in employment with a third party, also known as the efficiency margin(doelmatigheidsmarge). From 2023, the efficiency margin will be abolished and the salary must therefore be at least equal to that of someone with the most comparable employment. This could therefore result in a salary increase and additional payroll tax to be paid by director-major shareholders before 2023.

Restriction on borrowing from own company

The possibility to borrow from one’s own BV will be restricted as of 2023, in connection with the entry into force of the Excessive Borrowing from Own Company Act(wet excessief lenen). If a shareholder borrows more than € 700.000 from his or her own BV, the excess will be taxed in box 2 (once). The first tax reference point is 31 December 2023. First home equity debts do not count towards the € 700.000 limit if they are covered by a notarial mortgage deed (a mortgage deed is not required for home equity debts existing as of 31 December 2022). In the case of high loans or overdrafts, it is important to anticipate this and start repayments in advance, or reserve money for the tax settlement. Specific rules also apply in partner situations. Is your debt to the BV higher than € 700.000 or were you planning for this? Contact our office to discuss the possibilities and consequences.

Loss relief corporate income

Currently, companies can offset losses against profits from the precious year or the six consecutive years. No maximum amount applies. From 2022, up to €1.000.000 of the profit can be offset against losses. Only 50% of the profit that exceeds €1.000.000 be set off against tax losses. In addition, the time limit of 6 years will be cancelled; losses can be settled indefinitely. Unfortunately, the restriction applies to all Dutch companies, regardless of whether these losses originate from abroad. For small companies, the longer term for loss set-off may actually be an advantage.

Bill to prevent tax avoidance for international companies

In addition to the aforementioned bills on the Tax Plan, the following two bills have been submitted to the House of Representatives to tackle mismatches and tax avoidance in international structures:

– Bill on ‘Combating mismatches in the use of the arm’s length principle’: adjustment of the rules of arm’s length transfer pricing between international groups in order to prevent tax mismatches. In short, this bill means that a reduction of taxable profit is only permitted if this is deducted by an increase in the foreign tax base;

– Bill ‘Implementation tax liability measure from the second EU anti-tax avoidance directive’: the tax liability for reverse hybrid entities. In short, this proposal means that under certain circumstances the country of residence follows the qualification of the country where the participants or shareholders are established.

UBO register temporarily out of public access

The EU Court of Justice recently ruled that that the provision in the European Anti-Money Laundering Directive, which requires Member States to ensure that any member of the general public must have access to UBO information, is insufficiently substantiated and therefore invalid. Making the information of UBOs publicly accessible constitutes a serious interference with the right to privacy, according to the Court. As a result, the obligation that the UBO register be accessible to everyone is in question. In response, the government has decided that pending further decision-making, the Chamber of Commerce will temporarily stop providing information from the UBO register.

The above does not affect the duty for legal entities to register UBOs. Since 27 September 2020, it is mandatory for (many) entrepreneurs to register a UBO in the UBO register. UBO stands for Ultimate Beneficial Owner. These are individuals who own more than 25% of the shares or hold the economic interest or have effective control of the company.

Other tax tips

Do you expect to pay tax for the tax year 2023? If you request a provisional assessment in good time, this will save you tax interest. The tax rate for income tax entrepreneurs is currently 8%.

Did you find out that you forgot to include some items in your VAT return? Then submit a supplement declaration. You can do this for this year or for the past 5 years. If it concerns VAT to be received or remitted of € 1.000 or less, this is allowed to be included in the next VAT return. You do not need to submit a separate supplementary declaration for this.

Do you drive a company car and do you use this car privately? In that case, a correction must be made for private use in the last VAT return (to be submitted in January 2022). This may be based on actual use or on the basis of a fixed rate. Do you have questions about this? We are happy to help you.

If you have made sufficient investments to qualify for the small-scale investment deduction, but have not yet paid all investments, we advise you to make these payments before the end of the year so that you are eligible for the small-scale investment deduction. You are eligible for the small-scale investment deduction when the total investment is higher than € 2.400.–.

Has your partner worked in your business this year but has not received compensation yet? Then consider paying compensation before the end of the year. This is deductible in your business. For your partner, this reimbursement is taxable in box 1. The rate depends on your partner’s total Box 1 income and is especially advangtageous if your partner has a low income.

From 1 January 2025, the BPM exemption for company vans will be abolished. However, the exemption will continue to apply to vans purchased before that date. So if you were planning to purchase a van for your business anyway, it will be advantageous if this takes place before 1 January 2025. However, the BPM exemption will continue to apply to emission-free vans.

Additional measures have been announced regarding repayment of corona tax debts. We ask you to contact us for further clarification.

Among the various organisations we support, our financial support to the RRT Rapid Relief Team is the most current. RRT provides hope and support to people over the whole world – especially in the hour of need, such as the current war in Ukraine.

J.C. Suurmond & zn. Taxconsultants are happy to contribute to Operation 322, which RRT launced, to provide the homeless with care products and emergency food kits. RRT is currently loading trucks with food boxes and care kits for the Ukrainians. Volunteers throughout the whole of Europe are getting together to give aid to the refugees.

We are delighted to help the RRT Rapid Relief Team in making a difference!

We would like to inform you about the latest tax changes and saving opportunities with this end-of-year newsletter. We hope you will benefit from this newsletter. Please contact our office for more information and personal advice. We have distinguished our tips and hints between Individual and business. Please go ahead and read what applies to your situation!

Tax plan summary

As expected, the current outgoing government will not come up with any sensational plans for 2022. The plans largely concern previously taken decisions and smaller changes. The more notable changes are, for example, the abolition of the personal tax deduction for educational expenses and the arranging of a work from home allowance. Furthermore, the first bracket in the corporate income tax will be extended from € 245,000 to € 395,000. For 2023, the percentage of tax deductions in the Income Tax will decrease again by 3%; if it is possible to bring forward deductible expenses, the deduction will yield more this year. The plans are not final yet, as the Eerste Kamer(Dutch Upper House) has yet to vote on them.

Individual

Index individual fiscal tips

New Income Tax rates

Reduction in the rate of deductible items for higher incomes

30% ruling end

Replacement deduction for training costs

Changes in primary residence scheme

Transfer tax

Rent allowance

Change in income-related combination discount for foreign workers

Save tax in box 3 with an OFGR or BV

Take advantage of the annual gift tax exemption

Provisional assessment

Saving tax in box 3

Other tax tips

New income tax rates

There are no substantial changes in the Income Tax rates, only minor deviations and inflation adjustments.

Box 1 – Income from work and home

In 2022, the rate in the first bracket will be reduced from 37.10% to 37.07%. The threshold for the first bracket has also been raised this year, from € 68,507 to € 69,398. The rate for the second bracket remains 49.50%. After 2022, the basic rate will be further reduced step by step to 37.03% in 2024. Below is a schematic representation of the income tax in box 1 in 2021 and 2022.

A three-bracket system still applies to taxpayers who have reached the state pension age. Disc 1 goes from 19.20% to 19.17%. The second bracket goes from 37.10% to 37.07% and the third bracket remains 49.50%. Below is a schematic representation of the income tax in box 1 in 2021 and 2022.

Box 2 – Income from a substantial interest (for example a BV)

The rate for income from a substantial interest remains 26.9%.

Box 3 – Benefits from savings and investments

There is as yet no prospect of taxation on the assets in box 3 over the actual income.

In 2022, the tax-free allowance will be increased from € 50,000 per person to € 50,650 per person (€ 101,300 for tax partners).

In 2021, the rate on the notional return in box 3 has been increased to 31%. This rate will not be adjusted in 2022.

Below is a schematic representation of the capital gains tax in 2021 and 2022.

Reduction in the rate of deductible items for higher incomes

As already mentioned in 2020 and 2021, the highest rate at which virtually all deductible items are to be deducted is gradually being decreased. It can therefore be advantageous to bring forward deductible costs where possible. Taxpayers whose income falls in the highest bracket in box 1 will gradually have less tax advantage from these deductible items. In 2022, these deductible items may be deducted at a maximum of 40%, compared to 43% in 2021.

This percentage will be further reduced to the level of the first bracket, 37.03% in 2024. This concerns the following deductions:

Alimony

Deduction of training expenses (only in 2021, see separate chapter)

Deduction of expenses for specific healthcare costs

Deduction of weekend expenses for disabled

Gift deduction

Mortgage interest deduction

Entrepreneurial deduction (self-employed deduction, research and development deduction, cooperation deduction, starter’s deduction in the event of incapacity for work, discontinuation deduction)

Profit exemption for small and medium-sized businesses

Due to this reduction, the deductible items will yield more in 2021 than in 2022 and the following years. If your income falls in the highest tax bracket in 2021, it is therefore advisable, if possible, to pay deductible items such as gifts or healthcare costs before the end of the year.

30% ruling

Did your 30% ruling end on January 1st 2021? This means that your take-home salary has been lower. Also, you have become regularly taxable in the Netherlands for your worldwide assets and you will have to declare these in your 2021 tax return. You can read our tax tips regarding saving in Box 3 to see how you can minimize your Box 3 tax.

Replacement deduction for study costs

From the tax year 2022 onward, study costs are no longer deductible from the income tax. The tax deduction will be replaced by the STAP budget subsidy scheme (Incentive for the Labor Market Position). This budget will apply to people with a link to the Dutch labor market. From 1 March 2022, workers and job seekers can apply for a STAP budget at the UWV. This is possible per person once a year. The budget is €1,000 per person per year. If the application is approved, the amount is paid to the trainer. Only study costs paid in 2021 can still be deducted in the 2021 income tax return.

Changes in primary residence scheme

From 2022, the primary residence scheme will be adjusted in 3 parts. The scheme is being adjusted because unintended deduction restrictions occurred in marriage and partnership, which sometimes meant that less mortgage interest could be deducted. This occurred, for example, in people who bought a house with a partner, but had previously bought a house themselves (and had sold it with equity). Or with people who have a primary residence and of which one of the partners dies. It is adjusted for the components: home acquisition reserve, repayment position and home acquisition debt. If this applies to you, we are happy to provide further explanation.

Property transfer tax

It is important to take into account unforeseen circumstances before transfer at the notary! The start-up exemption has been introduced from the year 2021. First-Time Buyers between the ages of 18 and 35 (under certain conditions) do not pay a one-off transfer tax for their own home. Buyers from the age of 35 who are going to live in the house themselves pay 2% transfer tax. Buyers who are not going to live in the house themselves pay 8% transfer tax. It had already been arranged that in the event of unforeseen circumstances buyers could pay the 2% transfer tax and not the 8% after transfer at the notary, but nothing had yet been arranged for the period between the purchase and transfer at the notary. This will now also be taken into account from 1 January 2022. For example, if the buyers would divorce before the transfer at the notary, but after signing the purchase contract, and as a result, they will not live in the house themselves? Then they only have to pay 2% transfer tax and not 8%.

Rent allowance

The cabinet wants renters to receive or keep rent allowance more often. The current conditions will be relaxed on two points. From 1 January 2022, the application for a residence permit for children up to the age of 18 is no longer a condition for entitlement to housing benefit. In addition, from 1 January onward, the right to rent allowance in the event of exceeding the rent limit will be reinstated. Renters will again be eligible for housing benefit if their income or assets fall again and if they were entitled to housing benefit in the past regarding their house.

Change in income-related combination discount for foreign workers

The income-related combination discount can be applied to people with children under the age of 12. The conditions are that both partners work. For people who work in the Netherlands but live abroad, a partner who lives abroad does not count as a tax partner in the Netherlands. As a result, there was an unintended entitlement to the income-related combination tax credit in the past. From 2022, the partner abroad will now also be included to check whether they are entitled to this tax credit. The income-related combination discount will be reduced from a maximum of €2,815 to €2,534.

Save tax in box 3 with an OFGR or BV

If you have substantial assets and therefore pay tax in the higher box 3 brackets, it could be an option to set up an OFGR or BV to save box 3 tax. If you transfer the capital to this entity, this capital will be taxed in the corporate income tax and substantial interest taxation for the actual return on this capital.

The advantage is that this capital is then no longer taxed in box 3 at a (high) notional return. This is especially beneficial for low-yielding assets such as savings accounts. We recommend that you first discuss the options with an adviser to see whether this will benefit your situation.

You can also save on box 3 taxation by reducing the balance before the reference date of 1 January, for example by bringing forward expenses, mortgage repayment, annuity deposit, or payment of health insurance.

Take advantage of the annual gift tax exemption

Have you not yet made use of the annual gift exemption this year? You have until 31 December to make these donations. Please note that the money must be credited to the recipient’s account by December 31, 2021 at the latest. In 2021, the annual tax-free amounts will be temporarily increased by € 1,000 due to the Corona crisis. There is a general exemption of € 3,244. An exemption of € 6,604 applies to gifts to children. In addition, there are a number of one-off gift exemptions (for example, for a study or the purchase of a primary residence). If you have any questions regarding these exemptions, we will be happy to assist you.

Provisional assessment – recommended if you receive several pensions

If you receive a pension from several pension institutions, you often have to pay an additional amount in income tax when you file a return. This is caused by the fact that your total income falls in a higher bracket due to the various pensions. The pension authorities are not aware of your total income and only withhold tax on the amount they pay you. As a result, it is possible that too little wage tax has been deducted from the pensions and that you have to pay extra. You can request a provisional assessment to limit tax interest and to be able to pay the amount of income tax in installments. Do you think this situation applies to you? Or are you retiring soon? Please contact our office. We would be happy to see if it is wise to request a provisional assessment from the Tax Authorities.

Saving tax in box 3

The reference date for taxed box 3 assets is January 1. Here are a few tips to reduce your assets as of 1 January.

Do you plan to make major expenditures soon? Such as, for example, the purchase of a car, renovation of a house or consumer goods. Then it might be wise to make the purchase before 1 January. In this way you reduce your taxable assets.

You can use your savings to pay off part of the mortgage on the primary residence (box 1). In addition to wealth tax, this often also saves you some mortgage interest. Ask your mortgage lender about the conditions in order to prevent/limit penalty interest. Have you received a provisional refund in connection with the mortgage interest? Do not forget to adapt this to the new situation.

If possible, you can ask your health insurer whether it is possible to pay the health care premium in one go (before 1 January) instead of paying in installments. You often also receive a small discount for paying the premium all at once.

It can be beneficial to have small debts (together below the threshold of € 3,200 per taxpayer) repaid before January 1. In this way, the box 3 income is reduced and further interest on these loans is also avoided. Interest on personal loans is usually high and this interest is not tax deductible.

Deposit money into an annuity. Money that has been deposited as an annuity is no longer taxed in box 3. A deposit is worth considering, especially in the event of a pension shortfall. There are conditions attached to this.

If you have not yet made any donations this year, you can consider making them before 31 December.

Other tax tips

Do you expect to pay tax for the 2021 or 2022 tax year? Request a provisional assessment in good time, this will save you tax interest. You pay tax interest if the assessment is imposed later than 6 months after the end of the calendar year (1 July 2022). The tax interest is at least 4%. To ensure that the assessment is imposed in time, we recommend that you apply for it before 1 April 2022. The assessment for the 2021 tax year must be paid at once. There is the possibility of paying the assessment for the tax year 2022 in installments. Do you have questions about this? We are happy to assist you in applying for a provisional assessment.

If you expect to receive a refund for 2016, an Income Tax return for this year must be submitted before December 31, 2021. In 2022, the 5-year term for submitting this declaration will expire.

If possible, bundle deductible expenses such as medical expenses and donations in one specific year. For example, a deduction is achieved earlier and the threshold is only deducted once from the expenses. For donations, the threshold disappears completely if you commit the donation to a charitable institution for 5 years.

If your capital in the bank is higher than € 100,000, you may be confronted with negative interest. To avoid this, you can divide your money among several banks. Do ask for the conditions at the various banks. Negative interest may already be calculated for an amount lower than € 100,000.

Business tax tips 2021

Last year, the plans for an investment discount for SMEs (the BIK scheme) ultimately did not go ahead. This plan was to replace the cancellation of the plan to reduce the corporate income tax rates. This is probably due to the large expenses that the government has had to spend in order to support businesses during the corona crisis. We hope the reduction in corporate income tax for SMEs will eventually yet take place. For next year, however, an increase is planned in the second bracket from 25% to 25.8%. The first bracket in the corporate income tax has been extended from € 245,000 to € 395,000.

This extension benefits SMEs. As a result, doing business in a BV becomes more interesting for profits of up to nearly € 400,000.

Index business tax tips:

Change in box 2 and corporate tax

Increasing of support rates in the Environmental Investment Allowance (MIA)

Introduction of tax-free work from home allowance

Increase tax-free reimbursement

Stock options become more attractive as a remuneration

Private use electric car

Excessive debts of a shareholder to his own BV

Loss relief corporate income

Simplification of the one-stop-shop system in the VAT rules for e-commerce

Bills to prevent tax avoidance for international companies

UBO register

Other tax tips

Corona measures

Change in box 2 and corporate tax

The rate in box 2 will not be changed this year. This concerns income from a substantial shareholding, such as dividends and capital gains on equity interests above 5%. The rate remains 26.9%.

The corporate tax rate will be increased this year. Apart from that, the tax brackets are also modified. The corporate tax rate was 15% on the first €245,000 profit and 25% for profits above €245,000 this was 25% in 2021. In 2022, the rate will be 15% on the first € 395,000. The rate for profits above € 395,000 will be increased to 25.8%.

Increasing of support percentages in the Environmental Investment Allowance (MIA)

The government wants to minimize pollution and is therefore making environmentally-friendly investments more attractive for companies. The environmental investment deduction (MIA) allows companies to deduct a percentage of the investment costs from the taxable profit. As of January 1, 2022, the support percentages in the Environmental Investment Allowance will be increased. The support percentages were 13.5%, 27%, and 36%. The proposal is to increase these percentages to 27%, 36%, and 45% respectively.

Introduction of tax-free work from home allowance

Because many people have been working from home since the corona crisis (and this indirectly costs the employee money; more energy consumption, coffee consumption, etc.), the cabinet has decided to introduce a tax-free working from home allowance. As a result, employers can reimburse a maximum of € 2 per day or part of a day worked. The tax-free travel allowance of € 0.19 per km will continue to exist. Despite the rising prices of petrol and diesel, the travel allowance will not be increased but will remain at € 0.19 per kilometer. The fees cannot be paid at the same time; per day you can either opt for payment of the work from home allowance or payment of the travel allowance.

An employer may already provide a tax-free allowance for setting up a home workplace. The employer can reimburse the costs for, for example, an office chair or computer screen via other specific exemptions from the work-related costs scheme.

Increase tax-free reimbursement

Employers may reimburse certain expenses to their employees tax-free up to a maximum percentage of the total wage sum. In the context of the corona support measures, the maximum tax-free reimbursement to employees has been temporarily increased from 1.7% to 3% over the first € 400,000 of the wage sum. This temporary measure has been extended for the 2021 tax year. Do you still want to make use of this? Then you are still up to and including 31 December 2021 to reimburse the employee for certain costs tax-free. A bonus can also be paid out under this arrangement if this is customary (partly depending on the amount of the bonus). In 2022, the free space will be reduced again to 1.7% over the first € 400,000 of the wage sum and 1.18% on the excess. This arrangement comes in addition to expenses that are tax-free anyway, such as claiming business mileage at € 0.19 per km. Please contact your advisor for further information about the conditions.

Stock options become more attractive as a remuneration

Employers can offer their employees stock options as remuneration instead of paying them wages. This mainly occurs in companies that have just started (startups), because they do not yet have enough money to pay an appropriate salary. With stock option rights, the employee is given the right to buy a certain number of shares at a predetermined price in a certain period. Currently, tax is levied when the employee converts the options into shares. The disadvantage of this, is that the employee has to pay tax now, while they are not always allowed to sell the shares, in order to have the cash to pay the taxes. The government’s proposal is that employees can now choose when they pay tax. In future, the employee would be able to choose: either pay tax when the shares are tradable (and therefore money is available) or pay tax when the options are converted into shares (as it is now in 2021 ). This bill has been deferred for further consideration, and it is not clear yet whether or when it will come into force.

Private use electric car

As announced last year, the fictitious amount for the private use (‘bijtelling’) of electric cars will be further increased. In 2022, this addition will be increased to 16% on the first € 35,000 (this was 12% on the first € 40,000) and 22% on the excess. From 2023, the proposal is to shorten the first bracket to € 30,000.

Excessive debts of a shareholder to his own BV

It was previously announced that borrowing from a private limited company by a shareholder is to be limited. This plan would be implemented from 2022 onwards. However, this has been postponed to 2023. In addition, the State Secretary has asked the House of Representatives to continue the discussion in connection with a broader discussion about the tax treatment of assets that is being held in the formation of a new cabinet. It is to be expected that a new government will come up with further details.

Regarding this plan, from 2023 onward, loans or current account amounts in excess of an amount of €500,000, would be taxed at the then applicable rate in box 2 (rate 2022: 26.9%). Under certain conditions, an exception applies to home loans. In the case of large loans or current account debts, it is important to anticipate this and start with repayments, or to reserve money for the tax settlement.

Loss relief corporate income

Currently, companies can offset losses against profits from the previous year or the six consecutive years. No maximum amount applies. From 2022, up to €1,000,000 of the profit can be offset against losses. Only 50% of the profit that exceeds €1,000,000 be set off against tax losses. In addition, the time limit of 6 years will be canceled; losses can be settled indefinitely. Unfortunately, the restriction applies to all Dutch companies, regardless of whether these losses originate from abroad. For small companies, the longer term for loss set-off may actually be an advantage.

Simplification of the one-stop-shop in the VAT rules for e-commerce

New VAT rules for e-commerce apply from 1 July 2021 onwards. This concerns Dutch companies that sell to consumers in other EU countries. The rules consist of a lower threshold for distance sales and a simplified VAT declaration via a one-stop shop system so VAT does not have to be paid separately in each EU country. The rules apply when the Dutch webshop achieves an annual turnover of € 10,000 or more with sales to consumers in EU countries outside of the Netherlands (Dutch VAT may be charged below this).

The thresholds for intra-EU distance sales per individual EU country have been abolished. There is now 1 joint threshold amount of € 10,000 on an annual basis. The entrepreneur has to keep an eye on the threshold amount every year. As soon as the limit of € 10,000 is reached, the local VAT rate of the country where the private customer lives, must be applied from that moment on. In the following year, the entrepreneur should continue to invoice the local VAT of the EU country. If the entrepreneur’s turnover in the year after that was below the threshold of € 10,000, then Dutch VAT may be charged again. The entrepreneur may also choose to continue to invoice with the local VAT rate of the EU customer. The foreign VAT return can be filed separately for each EU country, or via the one-stop-shop- system. This is a new system for submitting VAT returns in one return for multiple EU countries.

The rules have also changed for the import of products from outside the EU that are delivered directly to consumers in the Netherlands, which is called dropshipping. Due to the expiry of the exemption, Dutch VAT will have to be paid on this. Also for this arrangement, a simplified procedure is in place for import VAT declarations. If you have further questions about these regulations, please contact us.

Bills to prevent tax avoidance for international companies

In addition to the aforementioned bills on the Tax Plan 2022, the following two bills have been submitted to the House of Representatives to tackle mismatches and tax avoidance in international structures:

Bill on ‘Combating mismatches in the use of the arm’s length principle: adjustment of the rules of arm’s length transfer pricing between international groups in order to prevent tax mismatches. In short, this bill means that a reduction of taxable profit is only permitted if this is deducted by an increase in the foreign tax base;

Bill ‘Implementation tax liability measure from the second EU anti-tax avoidance directive’: the tax liability for reverse hybrid entities. In short, this proposal means that under certain circumstances the country of residence follows the qualification of the country where the participants or shareholders are established.

UBO register

Since September 27, 2020, it is mandatory for (many) entrepreneurs to register their UBO in the UBO register. The register was created to prevent illegal acts such as money laundering and terrorist financing being carried out with financial constructions. UBO stands for Ultimate Beneficial Owner. These are persons who own more than 25% of the shares, or economic interest, or actual control of the company.

The following companies must register a UBO in the UBO register:

Unlisted private and public limited companies(BVs and NVs)

Foundations(stichtingen)

Associations with full legal capacity/with limited jurisdiction but with a company (verenigingen)

Mutual insurance companies

Cooperatives

Partnerships: partnerships, general partnerships, and limited partnerships

Shipping companies

European Public Limited Companies (SE)

European Cooperative Societies (SCE)

European Economic Interest Groups that, according to their statutes, have their registered office in the Netherlands (EEIG)

Religious denominations

If the company was registered at the Chamber of Commerce before 27 September 2020, the UBO must be registered in the UBO register before 27 March 2022. If the company is registered with the Chamber of Commerce after September 27 2020, the UBO must be registered within one week of incorporation. If changes are made to the UBO data, this must also be changed in the register, no later than one week after the change has taken effect.

The UBO can be registered at the Chamber of Commerce by means of an online UBO statement. If you need help with this or have any questions about this, we will be happy to assist you.

Other tax tips

Do you have a lot of savings and your own BV? You may consider transferring your savings to the B.V. by means of a share premium deposit before the end of the year. If the deposit is made before the end of the year, you will no longer have to pay box 3 taxation on that amount in 2022. It is important that you are aware of the conditions and consequences.

Do you expect to pay tax for the tax year 2022? If you request a provisional assessment in good time, this will save you tax interest. The tax rate for income tax entrepreneurs is currently 4%. For corporate tax, this percentage is normally 8%, but this has been reduced to 4% due to the Corona crisis. From 1 January 2022, this percentage will (probably) be reset to 8%.

Did you find out that you forgot to include some items in your VAT return? Then submit a supplement declaration. You can do this for this year or for the past 5 years. If it concerns VAT to be received or remitted of € 1,000 or less, this is allowed to be included in the next VAT return. You do not need to submit a separate supplementary declaration for this.

Do you drive a company car and do you use this car privately? In that case, a correction must be made for private use in the last VAT return (to be submitted in January 2022). This may be based on actual use or on the basis of a fixed rate. Do you have questions about this? We are happy to help you.

If you have made sufficient investments to qualify for the small-scale investment deduction, but have not yet paid all investments, we advise you to make these payments before the end of the year so that you are eligible for the small-scale investment deduction. You are eligible for the small-scale investment deduction when the total investment is higher than€ 2,400.–.

Has your partner worked in your business this year but has not received compensation yet? Then consider paying compensation before the end of the year. This is deductible in your business. For your partner, this reimbursement is taxable in box 1. The rate depends on your partner’s total Box 1 income and is especially advantageous if your partner has a low income.

Corona measures

With the rising Covid cases and new lockdown measures, the government has revived some of the business support measures such as the NOW and TVL. The NOW (Emergency Bridging Measure for Employment) provides compensation for wage costs in the event of a loss of turnover in order to maintain as much employment as possible. The Fixed Cost Allowance, or TVL, helps SMEs to pay part of their fixed costs. Also, the deferral of tax payment deadlines has been extended until the end of this year under certain conditions. As the measures are based on the temporary lockdown measures, these change continually. Please check for the most recent updates at https://business.gov.nl/corona/financial-support-measures/corona-support-for-entrepreneurs-after-1-october-2021/

Beheer cookie toestemming

Wij gebruiken technologieën zoals cookies om informatie over uw apparaat op te slaan en/of te raadplegen. We doen dit met als doel om de beste ervaring te bieden en om gepersonaliseerde advertenties te tonen. Door in te stemmen met deze technologieën kunnen wij gegevens zoals surfgedrag of unieke ID's op deze site verwerken. Als u geen toestemming geeft of uw toestemming intrekt, kan dit een nadelige invloed hebben op bepaalde functies en mogelijkheden.

Functioneel

Always active

De technische opslag of toegang is strikt noodzakelijk voor het legitieme doel het gebruik mogelijk te maken van een specifieke dienst waarom de abonnee of gebruiker uitdrukkelijk heeft gevraagd, of met als enig doel de uitvoering van de transmissie van een communicatie over een elektronisch communicatienetwerk.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistieken

De technische opslag of toegang die uitsluitend voor statistische doeleinden wordt gebruikt.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

De technische opslag of toegang is nodig om gebruikersprofielen op te stellen voor het verzenden van reclame, of om de gebruiker op een site of over verschillende sites te volgen voor soortgelijke marketingdoeleinden.